For a long stretch, fixed income stopped behaving the way investors expected.

Rates were pinned near zero, duration risk was invisible, and “income” quietly became a return-free placeholder. Then 2022–23 arrived. Rates rose fast. Bond funds fell. Investors learned—often painfully—that bonds can lose money, and that liquidity and stability are not the same thing.

Today, something has changed.

Not dramatically. Not heroically.

But structurally.

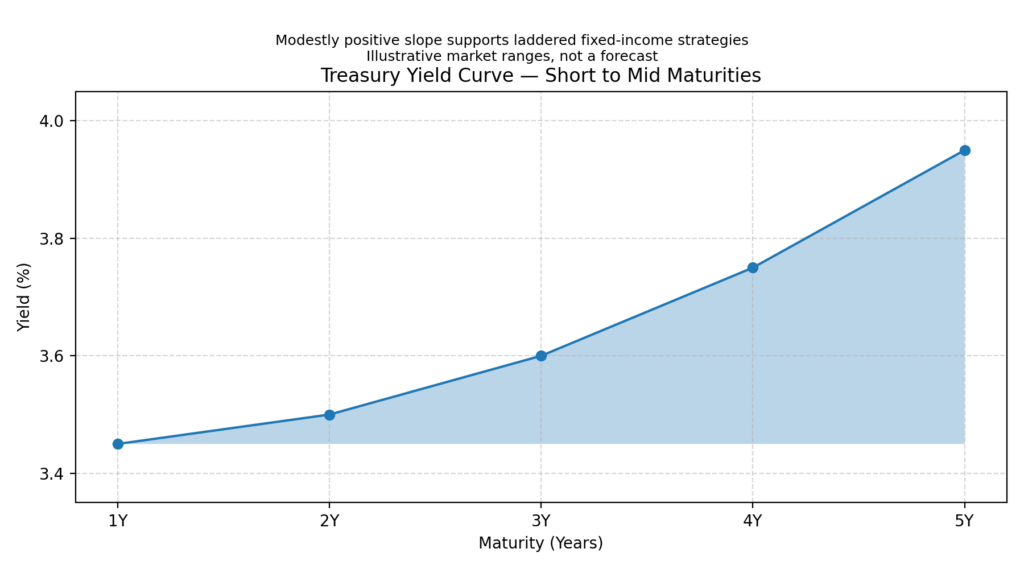

Across short to mid maturities, the yield curve has regained a modest positive slope. And that slope—quiet as it looks—is what makes laddered fixed income workable again.

This post explains:

- how bond ladders actually work,

- why individual bonds behave differently than bond funds,

- how to structure a real ladder for income,

- and how that structure holds up when rates, inflation, or markets move against you.

Most bond discussions still start with the wrong question:

“Where are rates going?”

Ladders flip that entirely. They start with a simpler, more useful question:

“When will I need this money?”

A bond ladder is not a rate call.

It’s a time allocation.

Instead of concentrating risk in one maturity or one fund, you spread capital across multiple maturities so that cash returns to you on a schedule—by design, not by sale.

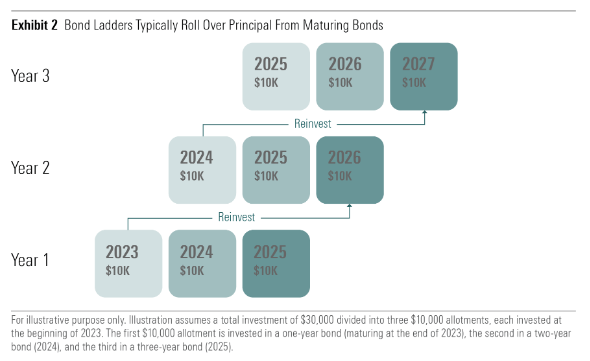

What a Bond Ladder Really is (Mechanically)

At its core, a ladder is just individual bonds with staggered maturities.

For example:

- a 1-year bond

- a 2-year bond

- a 3-year bond

- and so on

Each bond:

- pays contractual coupons,

- returns principal at maturity,

- and does not need to be traded to fund spending.

That last point matters more than most investors realize.

Why Individual Bonds Behave Differently Than Bond Funds

This distinction is where most confusion starts.

Bond funds:

- never mature,

- maintain constant duration,

- fluctuate daily in price,

- require selling shares to access cash.

Individual bonds:

- mature on a known date,

- naturally shorten in duration over time,

- return par value at maturity (assuming no default),

- provide liquidity without selling into the market.

Same asset class.

Very different experience.

Ladders are about cash-flow certainty, not mark-to-market comfort.

Why This Matters Now

In today’s environment:

- cash pays reasonably, but temporarily,

- short-term yields can change quickly,

- mid-curve yields are still lockable.

A modestly upward-sloping curve allows investors to:

- earn more than cash,

- without stretching credit,

- without making a long-duration bet,

- and without needing to be right about the Fed.

This is not an “opportunity” story.

It’s a structure story.

What Happens When Things Don’t Go as Planned?

This is where structure matters most.

- If interest rates fall:

Your near-term income doesn’t change. You already locked it in. - If interest rates rise:

You don’t need to sell anything, and future income may even improve. - If markets are volatile:

Your spending money isn’t tied to daily market prices.

This doesn’t remove all risk. But it removes the kind of risk that forces bad decisions.

This approach is about:

- predictability,

- planning,

- and peace of mind.

Disclaimer: Nothing here should be considered investment advice. All investments carry risks, including possible loss of principal and fluctuation in value. Finomenon Investments LLC cannot guarantee future financial results.