How to Use the Mega Backdoor Roth and Roth Conversions to Build Tax-Free Wealth

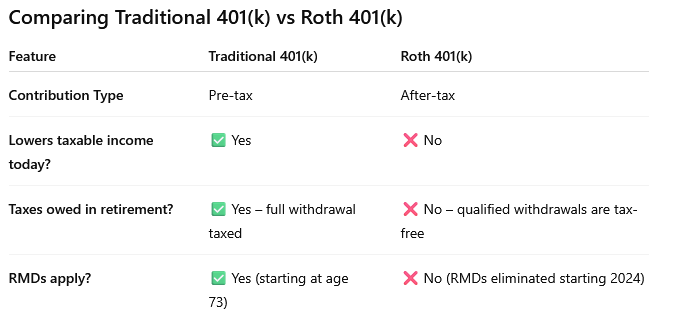

When planning for retirement, one of the key decisions employees must make is whether to contribute to a Traditional 401(k) or a Roth 401(k)—or a combination of both. While both accounts fall under the same annual IRS contribution limit ($23,500 for 2025, or $30,000 if age 50+), their tax treatment, timing, and long-term implications differ substantially.

Understanding the trade-off comes down to this: would you rather get a tax deduction today and pay taxes later in retirement, or pay taxes today and enjoy tax-free withdrawals later? The decision depends on your current vs. expected future tax bracket, your income trajectory, and your broader financial plan. Rather than viewing Traditional vs. Roth contributions—or Mega Backdoor Roth vs. Roth conversions—as mutually exclusive choices, sophisticated planning often blends them through multi-phase tax diversification strategies.

Roth accounts are one of the few remaining tax advantages that allow for truly tax-free growth and withdrawals. But for high-income professionals, direct access to Roth IRAs is often blocked by income limits. Even Roth 401(k) contributions are capped far below what many are capable of saving.

In this blog, we break down the mechanics of each—the Mega Backdoor Roth and the Roth Conversion strategy—so you can understand how they work, when to use them, and how to combine them effectively for long-term tax optimization. First, What’s the Difference Between Traditional and Roth 401(k)?

Why Consider Roth Strategies at All?

Because Roth accounts give you future tax-free income. That’s a big deal especially if:

You expect your income or tax rates to rise over time, even if your marginal tax rates fall due to lower income.

You want flexibility in retirement (Roth IRAs don’t have required minimum distributions).

You’re planning for decades of compound growth, allowing growth assets to be withdrawn last sequentially (your financial plan withdrawal strategy)

But Roth accounts come with contribution limits. And that’s where the Mega Backdoor Roth and Roth Conversions come in. There are two strategies, often confused but fundamentally different:

Mega Backdoor Roth – A way to put more post-tax dollars into Roth using after-tax contributions inside your employer sponsored 401(k) plan.

Roth Conversion – A way to shift existing pre-tax 401k dollars into Roth (Roth 401k or Roth IRA) by recognizing taxable income strategically.

Each has a place. But they are not interchangeable.

Prerequisites to Use the Mega Backdoor Roth Strategy

Before you go down the Mega Backdoor Roth path, make sure your employer’s 401(k) plan supports the required features. Not all plans do, and without the right setup, this strategy doesn’t work.

1. Your Plan Must Allow After-Tax (Non-Roth) Contributions

This is non-negotiable. The Mega Backdoor Roth hinges on your ability to contribute after-tax dollars above the $23,500 elective deferral limit. .

Check with your plan administrator: Does my 401(k) plan allow after-tax (non-Roth) contributions?

If your plan doesn’t support this after-tax account, the strategy is not available

2. Your Plan Also Must Allow Either:

In-Plan Roth Conversions (from after-tax 401(k) to Roth 401(k)), or

In-Service Withdrawals (from after-tax 401(k) to a Roth IRA)

If neither of these options are available, you’ll be stuck with after-tax dollars inside the plan that will grow tax-deferred—not tax-free. Worse yet, when you withdraw them, earnings will be taxed as ordinary income, not capital gains—potentially making it less tax-efficient than just investing in a regular brokerage account.

Check with your plan administrator: Can I convert after-tax 401(k) dollars to Roth 401(k), or roll them to a Roth IRA while still employed?

Why This Matters

When done correctly, the Mega Backdoor Roth allows you to shift after-tax dollars into Roth accounts annually – giving you the benefit of tax-free growth and withdrawals. But without the two plan features, the mechanics break down.

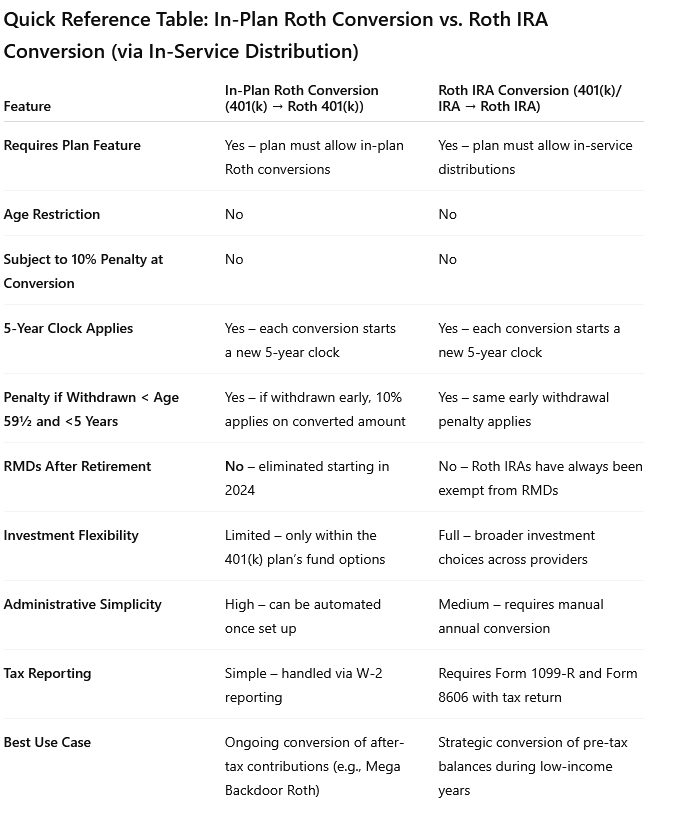

Which Method Should You Use?

There are two possible execution paths:

In-Plan Roth Conversion – converts your after-tax 401(k) dollars into Roth 401(k) inside the employer plan.

In-Service Rollover – rolls your after-tax 401(k) dollars to a Roth IRA (outside employer plan) while you’re still working.

While both are valid, most people should prefer the in-plan conversion method, if available. Why?

It can often be automated through payroll or plan settings.

It avoids the additional tax and administrative complexity of periodic rollovers to a Roth IRA outside employer plan.

You keep your assets consolidated within the 401(k) plan for better management and control.

If your plan allows it, set up automatic after-tax contributions and automatic in-plan conversions—the most seamless way to execute the Mega Backdoor Roth each year.

Table: Key Differences Between In-Plan Roth Conversions and Roth IRA Conversions (via In-Service Distribution)

Strategy Part 1: Mega Backdoor Roth – A Way to Put More Money Into Roth

The Core Problem

The IRS limits how much you can put into Roth each year in your employer sponsored plan.

In 2025:

You can only contribute a total of $23,500 to a Roth 401(k)or Traditional 401(k) – both have same deferral limit.

The total 401(k) contribution limit (including employer match and after-tax contributions) is $70,000 (or $77,500 if you’re 50+)

So there’s a $46,500 gap between what most people contribute and what’s possible (assuming no employer match in this example).

The Mega Backdoor Roth helps you fill that gap using after-tax contributions, and then convert those to Roth—legally and efficiently. This effectively bypasses Roth IRA income limits and 401(k) elective deferral contribution ceilings.

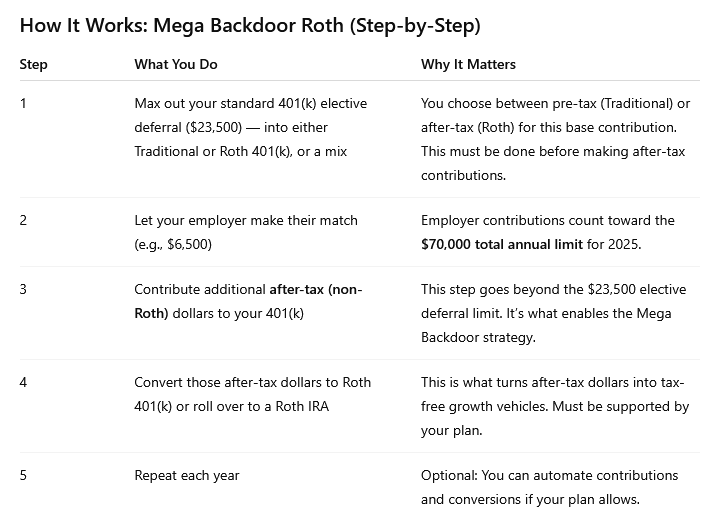

Example: What It Looks Like in Practice (2025)

Let’s say:

You contribute $23,500 to Roth 401(k) or Traditional Pre Tax 401k (You can contribute $23,500 to any one of those accounts inside your employer sponsored plan)

Your employer adds a $6,500 match as an example

You still have room to contribute up to $70,000 total.

That means: $70,000 – ($23,500 + $6,500) = $40,000 available for after-tax contribution

You add that $40,000 to your after-tax bucket in the 401(k), then immediately convert it to Roth 401(k) or roll it to a Roth IRA (a Roth IRA is your individual retirement account outside the employer sponsore plan). Note: The $6.5k employer match stays in Traditional 401(k). This is because the employer match cannot be made to your Roth 401k and hence that portion will sit inside your pretax 401k. aka traditional 401k.

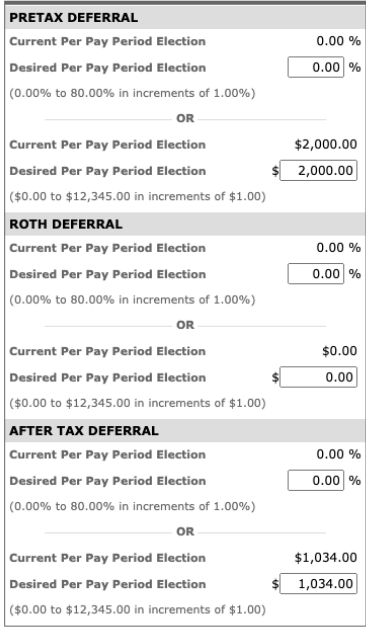

How To Execute This?

Login to your Fidelity 401(k). Once there, simply update the dollar amounts or percentages under each category—Pre-Tax, Roth, and After-Tax Deferrals—based on your strategy, then save your changes to begin funding your 401(k) as planned.

Sample Illustration of Contributions

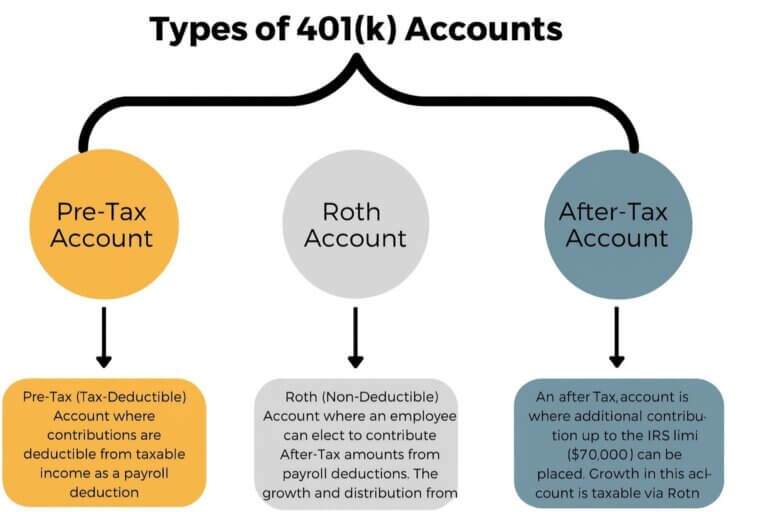

Pre-Tax Deferral: This is for your traditional 401(k) contributions, made with pre-tax dollars. The 2025 contribution limit is $23,500. These contributions reduce your taxable income today.

Roth Deferral: This is for Roth 401(k) contributions, made with after-tax dollars. You’ve already paid taxes on this income, so qualified withdrawals in retirement will be tax-free. In this example, we are not using this section, as the focus is on reducing current taxable income via pre-tax deferrals. The 2025 contribution limit is $23,500.

After-Tax Deferral: This section is where you contribute additional after-tax dollars beyond the $23,500 limit. These are the contributions used in the Mega Backdoor Roth strategy, allowing for future Roth conversion and tax-free growth.

If your plan allows it, set up automatic after-tax contributions and automatic in-plan conversions—the most seamless way to execute the Mega Backdoor Roth each year.

Important Note: If there is no “After Tax Deferral” section then, unfortunately, your employer doesn’t offer the Mega Backdoor Roth benefit.

Call Fidelity to Enable Automatic Roth In-Plan Conversions

Once your after-tax contributions are set up, you must call Fidelity Workplace Planning at 800-557-1900 and request to add “Automatic Roth In-Plan Conversion” to your account (If your plan supports it)

⚠️ Important: If this step is skipped, your after-tax contributions will remain in your traditional 401(k) account, where any future earnings will be taxed as ordinary income. This defeats the purpose of the Mega Backdoor Roth and can lead to unnecessary tax drag.

If the representative is unsure how to process your request, simply call again and speak with someone else—this is a known issue and may take persistence.

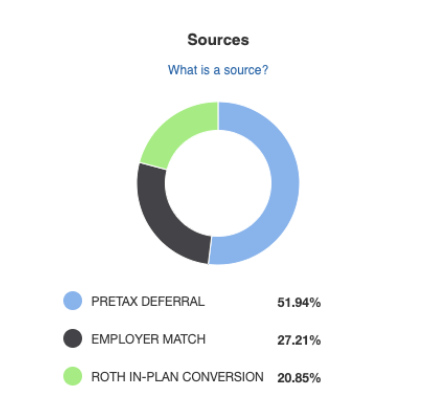

Verify That Your Mega Backdoor Roth Is Set Up Properly

After your next paycheck is processed, take the following steps to confirm that everything is working correctly:

a) Log into fidelity.com and go to your 401(k) account dashboard. b) Click on your 401(k) plan to open the account details. c) Look for the section titled “I Want To…” and click on “View Balances.” d) On the balances page, you’ll see a “Sources” pie chart. This will break down your contributions by type.

Fidelity Netbenefits> View Balances>Sources

If everything is working as intended, you should see an entry labeled “Roth In-Plan Conversion” showing a balance that matches your after-tax contribution. This confirms that your after-tax dollars have been successfully converted to Roth 401k within the plan.

Strategy Part 2: Strategic Roth Conversion

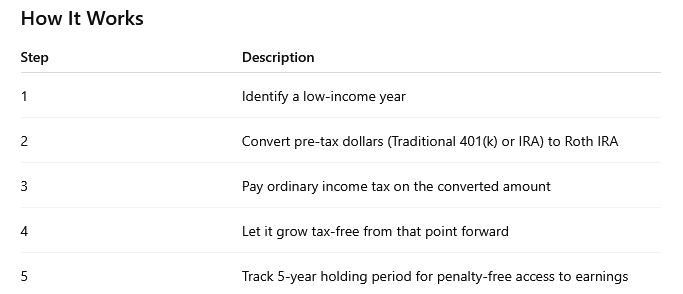

What is a Roth Conversion?

A Roth conversion means you move pre-tax retirement funds (Traditional 401(k) or IRA) into a Roth account (either Roth IRA or Roth 401(k)), and in doing so, you:

Pay ordinary income tax on the converted amount

Shift future growth into tax-free allocation.

The Core Problem

Over time, your Traditional 401(k) or IRA balance grows—and eventually, you’ll be required to take taxable distributions (RMDs) starting at age 73.

If most of your retirement savings are pre-tax, future withdrawals can:

Push you into a higher tax bracket

Increase Medicare premiums (via IRMAA)

Limit planning flexibility in retirement

Increase your lifetime federal tax liability.

Complicate inheritance and wealth transfer to heirs.

A Roth conversion allows you to move money from pre-tax 401k accounts to Roth (401k or IRA) accounts—by recognizing the income when your tax rate is low or manageable.

When It Works Best

You want to reduce future RMDs or create a tax-free inheritance

You’re in a sabbatical, gap year, or early retirement

You’ve temporarily dropped into a lower tax bracket

There’s no contribution limit. You can convert $5,000 or $500,000—so long as you’re prepared to pay the tax bill on the converted amount.

The goal: recognize income at today’s lower rates, rather than tomorrow’s possibly higher ones while accumulating growth assets lifetime tax free.

Used in isolation, each strategy is powerful. Used in coordination, they give you a full Roth playbook:

Use the Mega Backdoor Roth during your peak earning years to maximize Roth contributions while you’re earning is in surplus.

Use Strategic Roth Conversions in years where income drops—after a business sale, during early retirement, or when you exit a W-2 job.

Ultimately, this helps you build a more substantial Roth base—both through new contributions and smart conversions—enhancing your flexibility in retirement

This table provides a side-by-side comparison of Mega Backdoor Roth and traditional Roth Conversion strategies.

Summary: Why Both Strategies Matter for Tax-Efficient Wealth Building

The Mega Backdoor Roth and the Roth Conversion strategies are two of the most powerful, IRS-compliant tools available to high-income professionals who want to build long-term, tax-free retirement wealth.

Mega Backdoor Roth enables you to contribute well beyond the $23,500 deferral limit—up to $70,000 in 2025—by using after-tax contributions and converting them promptly into Roth (In plan or in service). It’s ideal during high-income working years when you’re still employed and want to create a growing base of tax-free retirement capital without income limits.

Roth Conversions, on the other hand, shine when you’re in a temporary low-income year—such as during a sabbatical, career change, or early retirement. They allow you to shift pre-tax dollars from Traditional 401(k) or IRA accounts into Roth IRAs, capturing future tax-free growth while locking in lower tax rates today.

Used in concert over a lifetime, these two strategies create a flexible, tax-optimized withdrawal plan, reduce future Required Minimum Distributions (RMDs), and expand your ability to manage tax brackets strategically in retirement.

In short, they’re not just clever tactics—they’re foundational tools for any high-income earner looking to reduce lifetime tax liability and build a more resilient, tax-diversified retirement portfolio.

If you are unclear about how to take the key steps to execute this strategy, book a call with your advisor for further help or guidance.

Disclaimer: This blog is intended for informational purposes only and does not constitute tax or investment advice. Please consult with your tax advisor before implementing any Roth-related strategy. IRS rules and limits change annually. All investments carry risks, including possible loss of principal and fluctuation in value. Finomenon Investments LLC cannot guarantee future financial results.

Shabrish Menon

Founder and CEO

Shabrish Menon loves finance and capital markets and shares deep insights that help clients make better and more informed decisions. Shabrish has built a reputation for delivering tailored financial advise that align with clients’ unique goals and risk profiles.

Finomenon Investments LLC is a registered investment adviser in the State of Washington. The Adviser may not transact business in states where it or its supervised persons are not appropriately registered, excluded or exempted from registration. Financial Advisors do not provide specific tax/legal advice and information should not be considered as such. You should always consult your tax/legal advisor regarding your own specific tax/legal situation. Finomenon Investments LLC cannot guarantee future financial results. Investment products are not insured by the FDIC, NCUA or any federal agency, are not deposits or obligations of, or guaranteed by any financial institution, and involve investment risks including possible loss of principal and fluctuation in value.

Scroll to Top

Disclaimer & Agreement

Finomenon Investments, LLC is an Investment Management and Financial Planning firm. Finomenon Investments LLC advises certain private individual clients and is a registered investment advisor only in the state of Washington. This website is a resource for audiences and should not be used as individual advice. Under no circumstances should any information presented on this website be construed as an offer to sell, or solicitation of any offer to purchase, any securities or other investments. This website does not contain the information that an investor should consider or evaluate to make a potential investment decision. Materials relating to investment and/or financial planning services provided by Finomenon Investments, LLC is not available to the general public through this resource.

To view this content, you must agree to the following terms, in addition to and supplementing the Finomenon Investments LLC Terms of Use and Privacy Policy:

I confirm to Finomenon Investments, LLC and agree that:

I am entering this website only to obtain general information and knowledge and not for any other purpose.

I understand that investments managed by Finomenon Investments, LLC are for private individuals who have unique individual risk tolerance, goals and financial profile.

I understand that this website does not contain the information I would need to consider for an investment.

I understand that when Finomenon Investments, LLC makes third party information available, Finomenon Investments will not have verified statements or claims made by third parties and will credit the relevant source where available.

I understand that third party materials such as YouTube videos or Charts referenced in blog posts or resources will not have been edited by Finomenon Investments and statements in those materials by individuals unassociated with Finomenon Investments LLC should only be understood in the context in which they were used.

The content constitutes the proprietary intellectual property of Finomenon Investments LLC. Prior written consent of Finomenon Investments LLC is required for distribution, copying or any modifications.