If you’re in your 20s or early 30s, taxes might feel like just another adult chore. But here’s the truth: how you handle your taxes now shapes how much wealth you build later.

Most young professionals focus on earning and investing—but overlook how much they lose to taxes. Not because they did anything wrong. But because no one told them how to do it better.

This post breaks down 10 simple, legal, and effective tax strategies you can use—without needing a CPA or a finance degree.

1. Choose the Right Type of 401(k)

When you contribute to your company 401(k), you often have two choices:

- Traditional 401(k): You get a tax break now. You pay taxes when you withdraw the money in retirement. Mandatorily so when you begin age 73 per IRS RMD rules.

- Roth 401(k): You pay taxes now. But all future withdrawals are tax-free. Roth accounts are also not subject to RMD rules.

When to use which:

- If you’re in a lower tax bracket today (like 12–22%), the Roth usually makes more sense.

- If you’re in a higher bracket and expect lower income in retirement, the Traditional 401(k) could be better.

- A multi-pronged strategy is likely more beneficial over a 20–30-year capital accumulation phase.

2. Convert to a Roth IRA in Low-Income Years

Did you take a sabbatical, go to grad school, or switch jobs recently?

Those “gap” years are perfect for a Roth conversion. This means moving money from a Traditional IRA to a Roth IRA and paying tax on it now—while your income is low.

Why it matters:

You lock in a low tax rate and allow your money to grow tax-free for life. It’s a one-time cost for a lifetime benefit. This needs to be planned with your CPA and Financial Advisor.

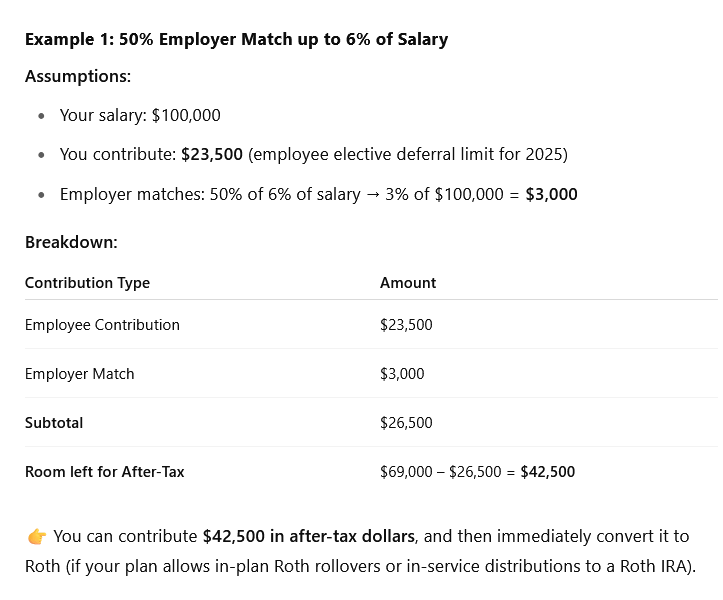

3. Use the Mega Backdoor Roth (If Offered)

Some employers (especially in tech) allow after-tax contributions to your 401(k), beyond the standard limit.

If so, you can:

- Contribute more than the $23,500 (2025 tax deferral limit).

- Convert those extra dollars to a Roth 401(k) or Roth IRA.

- Let them grow tax-free forever.

This is called the Mega Backdoor Roth.

And it can let you stash away up to $69,000/year (2024 limits) in retirement savings.

4. Make an 83(b) Election if You Join a Startup

If you get startup equity (real stock that vests over time), you may be eligible for an 83(b) election.

- It lets you pay income tax on the stock’s value now (when it’s worth very little).

- Later, when it grows in value, the gain is taxed as capital gains, which are usually much lower.

Caution: You only have 30 days from your stock grant to file this with the IRS. If you miss the window, you lose the benefit. Your tax eligibility is also defined via NSO, ISO grant type and qualification.

5. Open and Fund an HSA (Health Savings Account)

If your health plan qualifies, don’t skip this hidden gem.

- Contributions are tax-deductible

- Growth is tax-free

- Withdrawals are tax-free if used for medical expenses

Triple tax advantage—no other account offers that.

Bonus tip: Let it grow and pay medical expenses out of pocket now. Reimburse yourself years later for tax-free income.

6. Place the Right Investments in the Right Accounts

This is called asset location. It’s about putting your investments in the most tax-efficient places.

- Keep bonds or REITs (which generate a lot of taxable income) inside retirement accounts.

- Keep ETFs and index funds (which are tax-efficient) in taxable brokerage accounts.

It could quietly add 0.20–0.60% per year to your after-tax return. Approximations only.

7. Withdraw Your Money in the Right Order Later

When you retire (or take time off), the order you pull money matters:

- Tap taxable brokerage accounts first (lowest taxes now). You also control to sell long term for lower capital gains.

- Then use Traditional IRAs and 401(k) (taxed as regular income).

- Leave Roth IRAs for last—they grow tax-free and have no required withdrawals and compound most efficiently.

This strategy can reduce taxes over your lifetime and help manage Medicare or Social Security impacts later.

8. Harvest Investment Losses When the Market Drops

Tax-loss harvesting means selling investments at a loss to offset gains elsewhere. If your losses exceed your gains, you can deduct up to $3,000/year from your regular income.

Even better:

Unused losses roll over year after year, quietly reducing your tax bill in the future.

9. Use a Donor-Advised Fund for Smart Giving

If you’re charitably inclined and having a high-income year, consider a Donor-Advised Fund (DAF).

- You get a tax deduction now

- You can give the money to charities later

- You can donate appreciated stock instead of cash, avoiding capital gains tax

Pair this with bunching donations—grouping a few years of giving into one tax year to exceed the standard deduction threshold.

10. Don’t Miss Easy Tax Credits

Credits reduce your tax bill dollar-for-dollar—far better than deductions.

- Saver’s Credit: If you earn under ~$36,500 (single), you may qualify by just contributing to retirement.

- EV Credit: Up to $7,500 for buying a qualified electric vehicle.

- Energy Credit: For installing efficient home improvements like solar panels or heat pumps.

Tip: Always check for new credits each year. Tax law changes frequently.

Final Thoughts: Start Early, Save More

These strategies aren’t just for millionaires. In fact, they matter more when you’re early in your career. Why?

Because tax savings compound. The dollars you save today can grow over decades. But the window to act often closes fast—many of these moves must be done before the year ends.

If you’re a young professional earning well, building equity, and investing in your future, don’t leave tax savings on the table.

Want help applying these to your situation?

At Finomenon Investments, we help corporate professionals, startup employees, and growth-minded young earners optimize their money—not just invest it.

You’ve already started building income. Let’s help you build wealth, intentionally and tax-efficiently.

Disclaimer: Nothing here should be considered investment or tax advice. Please consult a qualified advisor or CPA before taking tax filing action. Finomenon Investments is a Registered Investment Advisor in Washington. As Fee Only Advisors, we are not affiliated with any Broker Dealer (BD), Bank or Family of Funds and serve as fiduciaries to corporate managers and executives.

Image Credit: Images used are not created by Finomenon Investments. Please share the source and author if known to help give credit.